What Costs Should You Expect When Downsizing in Texas?

If you are thinking about downsizing in Texas, it is easy to focus on one number:

What will I get for my current home?

That number matters, of course. But it is not the only number that matters.

A downsizing move can involve costs before the home ever goes on the market, costs during the sale, costs tied to the next purchase or rental, and costs that show up after the move when you are trying to make the new home work well for the next chapter.

That does not mean downsizing is a bad financial decision. In many cases, moving to a smaller, easier-to-manage home can reduce maintenance, physical burden, and long-term stress.

But the move usually works best when you understand the full cost picture ahead of time.

Especially if you are leaving a longtime home in Northwest Austin, Cedar Park, Round Rock, or elsewhere in Central Texas, the real question is not just:

“How much equity do I have?”

It is:

“What costs should I plan for so this downsizing move does not surprise me?”

Should You Hire a Senior Move Manager When Downsizing in Austin?

Why downsizing costs are often underestimated

A traditional move may be fairly straightforward. You pack, hire movers, close, and go.

Downsizing is often different.

It may involve:

deciding whether to sell as-is or fix things first

decluttering decades of belongings

donation pickups, junk removal, or estate sale help

preparing an older home for photography, showings, and inspection

coordinating a purchase, rental, leaseback, or temporary housing

understanding property tax changes

paying closing costs on the sale and possibly the next purchase

making the new home fit your life once you arrive

That is why the cost of downsizing is not just “moving expenses.”

It is a series of decisions, each with its own financial impact.

Should You Rent First After Selling a Longtime Home in Northwest Austin?

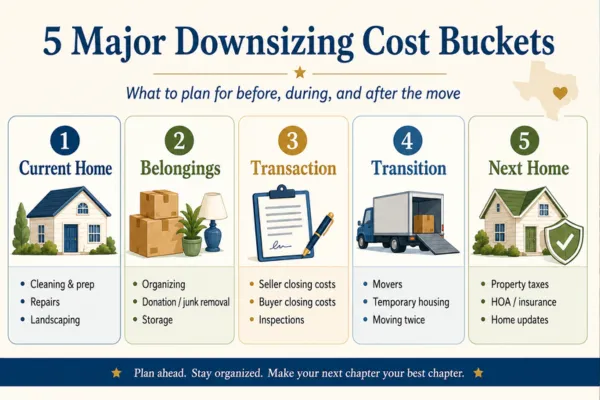

Cost category 1: Home preparation before selling

For many longtime homeowners, this is the first real cost category.

If your home has been lived in for 20, 30, or 40 years, it may need some preparation before it goes on the market. That does not always mean remodeling. In fact, it often should not.

But it may mean:

deep cleaning

decluttering

landscaping cleanup

paint touch-ups or interior repainting

carpet cleaning or selective flooring replacement

light fixture or bulb updates

pressure washing

minor handyman repairs

odor removal

hauling away items that will not move with you

The goal is not to make an older home perfect. It is to make it show as cared for, clean, and marketable.

The amount you spend here depends heavily on the condition of the home and your selling strategy. A seller planning to market a home as a strong move-in-ready option may spend more than a seller choosing an honest as-is or light-prep strategy.

Cost category 2: Repairs or inspection-related work

This is separate from cosmetic preparation.

Older homes may have issues that sellers need to think through strategically before listing, such as:

roof concerns

HVAC age or performance

plumbing leaks

electrical items

drainage or water-intrusion concerns

wood rot

windows or doors that do not function well

safety items like loose railings or trip hazards

Texas sellers generally need to address known material defects through proper disclosure, and as-is positioning does not eliminate disclosure considerations. That means it is often worth understanding potential condition issues before the buyer’s inspection forces the conversation under contract.

You may decide to:

repair an item before listing

obtain an estimate and price accordingly

disclose it and sell as-is

order a pre-listing inspection in some situations

Each route can affect your net proceeds and your stress level.

Cost category 3: Decluttering, organizing, and dealing with belongings

This is one of the most underestimated parts of downsizing.

If you are leaving a longtime family home, you may need help with:

professional organizing

sorting possessions

donation pickup

junk removal

shredding old documents

auction, consignment, or estate-sale coordination

transporting items to adult children

temporary storage during the transition

Some homeowners handle most of this themselves. Others decide that professional help is worth it because it saves months of delay and reduces family tension.

This cost is highly personal. A lightly furnished home may require very little. A home full of decades of belongings may require a real project budget.

Cost category 4: Senior Move Manager or downsizing support

Not everyone needs a Senior Move Manager, but some homeowners absolutely benefit from one.

This type of professional may help with:

planning the move

sorting belongings

coordinating donations or resale

helping adult children claim items

arranging movers

packing and unpacking

setting up the new home

The National Association of Senior & Specialty Move Managers describes this work as support for the physical and emotional aspects of downsizing, relocating, and simplifying a home.

If the move feels overwhelming, this may be one of the costs that buys back the most peace of mind.

Cost category 5: Moving expenses

Actual moving costs depend on:

how much you are moving

how far you are moving

whether you need packing help

whether heavy or delicate items are involved

whether you are moving once or twice

whether stairs, elevators, or difficult access are involved

A move from Northwest Austin to Cedar Park or Round Rock is not a cross-country move, but it can still be significant if you are transporting years of furniture, artwork, books, tools, and household goods.

If you sell first and rent before buying, or if you move into temporary housing, you may have two move-related cost events instead of one.

Cost category 6: Storage

Storage is often tied to one of three situations:

You need to declutter before listing.

You sell first and rent temporarily.

You are not ready to decide what to do with everything.

The first two can be sensible.

The third can quietly become an expensive delay tactic.

Storage may include:

monthly unit rental

climate-controlled storage

pickup and delivery

mover labor to load and unload

insurance or protection costs

If you are considering storage, ask yourself:

“Is this a short-term transition tool, or am I paying to avoid a decision?”

That one question can save a lot of money.

Cost category 7: Temporary housing or overlap costs

Some downsizers move directly from their longtime home into the next one. Others do not.

If your timing does not line up, you may face:

a short-term rental

apartment or furnished-housing costs

hotel stays in rare cases

a leaseback arrangement

overlap between two owned homes

overlap between rent and mortgage payments

This is why the questions “Should I buy before selling?” and “Should I rent first?” matter so much.

The right path is not always the cheapest one on paper. Sometimes paying for flexibility prevents a rushed next-home purchase that would cost far more emotionally and financially over time.

Cost category 8: Closing costs when you sell

Selling a home involves more than paying off a mortgage, if there is one.

Seller-side closing costs may include items such as:

title-related charges, depending on contract terms

escrow or settlement costs

prorated property taxes

HOA resale documents or transfer-related fees, if applicable

negotiated buyer concessions or repair credits

professional service fees tied to the sale

real estate compensation as agreed in the listing arrangement

The specific breakdown depends on the contract, local custom, the property, and negotiated terms. The key is to ask for an estimated seller net sheet early so you understand the likely proceeds before making next-step decisions.

Cost category 9: Closing costs when you buy the next home

If you are purchasing another home, buyer closing costs need to be part of the plan too.

The Consumer Financial Protection Bureau notes that mortgage closing costs can include appraisal fees, title-related charges, government taxes, prepaid homeowners insurance, prepaid property taxes, and interest through the first payment period, among other loan-related charges.

If you are buying with cash, you may avoid lender-related charges, but there can still be title, recording, inspection, survey, insurance, and other transaction expenses depending on the situation.

This is why your downsizing budget should not assume that the purchase price is the only cash need on the next home.

Cost category 10: Property taxes on the next home

This is one of the biggest potential surprises for Texas downsizers.

A smaller home does not automatically mean a smaller property tax bill.

Texas does not have a state property tax. Local taxing units set tax rates, and the taxable amount is affected by appraised value, exemptions, and local taxing entities.

If you are 65 or older, homestead and over-65 property tax rules may matter. The Texas Comptroller explains that age 65+ homeowners may qualify for additional residence homestead exemption benefits, but you need to understand how exemptions apply to the new home rather than assuming your current tax situation transfers automatically.

This matters if you are moving:

from Northwest Austin to Cedar Park

from Travis County to Williamson County

from one school district to another

from an older protected tax situation into a newer home with a different taxable value

Before buying, estimate the likely tax bill on the next home based on your expected exemptions and tax circumstances, not only the tax number shown on the listing.

Cost category 11: Financing changes, interest rates, and monthly payment tradeoffs

Some downsizers buy their next home outright after selling. Others finance part of it.

If you are financing, consider:

down payment

mortgage payment

interest rate

cash reserves after closing

whether proceeds are better used fully in the purchase or partly held for liquidity

whether a mortgage recast or other financing strategy may apply after your current home sells

This is not just a real estate question. It is a broader financial-planning question, and it is worth reviewing with a lender and, where appropriate, a financial advisor or CPA.

Cost category 12: Making the next home work for your life

A downsizing budget should not stop at closing.

Once you move, the next home may need:

window coverings

new furniture that fits the space

shelving or storage systems

a safer shower setup

grab bars or accessibility improvements

lighting changes

a new washer and dryer

updated locks or smart-home items

landscaping simplification

paint or minor refreshes before move-in

A home that is technically smaller may still need an upfront investment to become genuinely easier to live in.

This is especially true if you are moving from a longtime home where everything was already customized to your habits.

How to Prepare an Older Northwest Austin Home for Inspection Before Selling

The “hidden” cost: making the wrong move too quickly

This is not a line item on a closing statement, but it is real.

If you rush into the wrong next home because:

your current home sold faster than expected

you did not plan for temporary housing

you did not understand the cost of staying near family versus moving farther out

you underestimated your future tax bill

you bought a smaller home that still has too many stairs or too much maintenance

Then the long-term cost can be significant.

That is why planning matters.

The cheapest downsizing plan is not always the best one.

The best one is the plan that reduces the odds of regret.

How to Talk With Adult Children About Selling the Family Home

A practical downsizing cost checklist

Before selling, I would want longtime homeowners to think through these buckets:

Current-home preparation

cleaning

decluttering

repairs

landscaping

staging-related simplification

Belongings and transition support

organizer

Senior Move Manager

estate sale

donation pickup

junk removal

storage

Real estate and transaction costs

sale-related closing costs

purchase-related closing costs

inspections

appraisal, if financing

survey or title-related items as applicable

Housing overlap or timing costs

temporary rental

leaseback considerations

two-home overlap

second move if renting first

Next-home ownership costs

taxes

insurance

HOA dues

maintenance

modifications

furnishings or layout changes

Seeing the full list does not mean every homeowner will incur every cost.

It means you can plan instead of being surprised.

How Long Does Downsizing Usually Take in Austin? A Realistic Timeline for Longtime Homeowners

What I would caution downsizers not to do

Avoid these mistakes:

assuming a smaller home means lower total costs

ignoring property tax differences

remodeling the current home without a clear return strategy

moving belongings you already know you do not want

renting storage indefinitely

waiting until the last minute to deal with family items

forgetting closing costs on the next purchase

using the listing tax bill as your personal future tax estimate

underestimating how much it costs to make a new home fit your lifestyle

These are the places where otherwise smart plans get sloppy.

What to Do With a House Full of Stuff Before Downsizing in Northwest Austin

My practical take

If you are downsizing in Texas, I would divide the planning into three numbers:

1. What will it cost to leave well?

This includes preparing and selling the current home.

2. What will it cost to land well?

This includes buying or renting the next place, moving, and making it livable.

3. What will it cost to live there well?

This includes taxes, HOA dues, maintenance, insurance, and long-term fit.

When you understand all three, the decision becomes much clearer.

What Happens to Your Property Taxes When You Downsize in Texas?

Final thought

Downsizing can be financially smart, emotionally healthy, and practically freeing.

But it is not free.

The move may involve costs for preparation, belongings, movers, closing, temporary housing, taxes, and getting the next home set up properly.

None of that should scare you away from downsizing if the current home no longer fits.

It should simply push you to plan with your eyes open.

A good downsizing move is not just about reducing square footage.

It is about improving daily life without being blindsided by the cost of getting there.

Watch the Downsizing with Dignity Video Series

FAQ

What costs should I expect when downsizing in Texas?

Common categories include home preparation, repairs, decluttering, organizers or move managers, estate sale or junk removal, movers, storage, temporary housing, seller closing costs, buyer closing costs, property taxes, and updates needed in the next home.

Does downsizing always save money?

Not automatically. Downsizing may reduce maintenance and simplify life, but property taxes, HOA dues, closing costs, moving expenses, and next-home improvements can offset some of those savings.

Will my property taxes go down if I buy a smaller home?

Not necessarily. Texas property taxes depend on appraised value, exemptions, tax rates, and local taxing units. A smaller home can still have a higher tax bill in some circumstances.

Should I budget for repairs before selling my longtime home?

Usually, yes. Even if you do not plan a major renovation, you may need to budget for cleaning, landscaping, small repairs, or larger condition decisions that affect buyer confidence and pricing.

Are closing costs different when downsizing?

The costs are not unique to downsizing, but a downsizer may experience both seller-side costs on the current home and buyer-side closing costs on the next home. Mortgage-related buyer closing costs may include appraisal, title, taxes, prepaid insurance, and other charges.

What is the most overlooked downsizing cost?

For many homeowners, it is the cost of transition - decluttering, storage, moving twice, temporary housing, and making the next home actually fit the new lifestyle.