Should You Sell Your 78750 or 78759 Home Before You Downsize?

If you've owned a home in 78750 or 78759 for fifteen, twenty, or twenty-five years, you're sitting on something significant. The equity that has accumulated in a Northwest Austin home over that period is real, substantial, and - for many longtime owners in these zip codes - the single largest financial asset they have.

At some point, the question of what to do with that asset becomes a practical one. Maybe the house feels too big now that the kids are gone. Maybe the maintenance pile is growing faster than you want to deal with it. Maybe you're thinking about where you want to be in the next chapter and the current home doesn't quite fit that picture. Maybe you're watching neighbors downsize and wondering whether now is the right time.

This post is for the homeowner in 78750 or 78759 who is actively thinking about that question but hasn't made any decisions yet. It covers the financial picture, the tax situation that specifically affects longtime Texas homeowners, what the current market looks like from a seller's perspective, the sequencing question, and what usually separates downsizers who feel great about their decision from the ones who wish they'd handled it differently.

What Is the Best Order of Steps for Downsizing From a Longtime Home?

The Equity Position: What Longtime 78750 and 78759 Owners Are Actually Sitting On

The numbers here are worth stating plainly, because many longtime owners in these zip codes don't fully grasp what they've accumulated.

A home purchased in 78750 or 78759 in the late 1990s or early 2000s for $200,000 to $300,000 is worth somewhere between $500,000 and $800,000 or more today depending on size, lot, condition, and school assignment. A home purchased in the mid-2000s for $350,000 to $450,000 has similarly appreciated to a range that produces meaningful equity. Even accounting for the softening from the 2022 peak, the five-year, ten-year, and twenty-year appreciation curves in these zip codes have been consistent and significant.

What that means practically: a longtime owner in these zip codes who has paid down a meaningful portion of their mortgage and has a home worth $600,000 to $900,000 may be carrying $400,000 to $700,000 or more in net equity. For many of these homeowners, that equity has been quietly growing in the background of daily life without being actively thought about - and the decision of whether and when to sell is also a decision about whether and when to unlock it.

That equity can fund a next home outright or with a very small mortgage, cover a significant portion of retirement expenses, reduce carrying costs dramatically by moving to something smaller and lower-maintenance, or simply create financial flexibility that living in an illiquid asset doesn't allow.

The Tax Picture: What Texas Homeowners Need to Know Before They Sell

This is an area where longtime owners in these zip codes are often not fully informed, and where the specific Texas tax situation makes the calculus different from what owners in other states might assume.

First, the federal capital gains question. A married couple selling a primary residence can exclude up to $500,000 in capital gains from federal income tax under the current primary residence exclusion, provided they've lived in the home for at least two of the past five years. A single filer can exclude up to $250,000. For longtime 78750 and 78759 owners with substantial appreciation, this exclusion may cover the entire gain or cover most of it. The gain that exceeds the exclusion is subject to capital gains tax at either 0%, 15%, or 20% depending on your income level. This is not the place to get specific tax advice - that requires a conversation with a CPA who knows your full situation - but understanding that the exclusion exists and roughly how it applies to your situation is worth doing before you list.

Second, the Texas over-65 property tax benefits. Texas voters approved changes in late 2025 that took effect January 1, 2026, creating a significantly enhanced property tax picture for seniors. As of 2026, eligible Texas homeowners age 65 or older can stack a $140,000 general homestead exemption with a $60,000 over-65 exemption, for a combined $200,000 reduction in taxable value for school tax purposes. For many homes in 78750 and 78759, this combined exemption effectively eliminates school district taxes entirely.

The over-65 exemption also triggers a school tax freeze - your school district taxes are locked at the dollar amount you paid in the year you turned 65 and cannot increase regardless of how much your appraisal rises. That's a meaningful financial benefit for longtime owners planning to stay put.

But here's what matters specifically for downsizers: when you sell and buy another home in Texas, you can transfer the benefit of your school tax freeze to the new property. You do this by requesting a Tax Ceiling Certificate from your county appraisal district when you sell, then presenting it to the new county's appraisal district within one year of moving. The new ceiling is calculated proportionally based on the percentage you paid under your old ceiling. You don't lose the freeze by downsizing within Texas - you carry it with you. This is a specific Texas provision that many longtime owners don't know about and that significantly changes the financial math of downsizing.

The practical takeaway: if you have the over-65 exemption and school tax freeze on your current 78750 or 78759 home, get the Tax Ceiling Certificate when you close and apply it to your new home. If you're not yet 65 and you're thinking about selling in the next few years, the timeline of when you sell relative to when you turn 65 can affect which exemptions you carry into your next purchase. Have this conversation with your CPA before you make timing decisions.

Should You Move Closer to Your Adult Children When You Downsize?

What the Current Market Looks Like From a Seller's Perspective

The market in 78750 and 78759 right now is functional for sellers but requires more strategy than it did in 2021 and 2022. Homes in 78750 are averaging around 86 days on market, and the current median sold price is running around $535,000 - essentially flat year over year but down on a price-per-square-foot basis from recent highs.

For longtime owners with substantial equity, this market reality is different from what it is for sellers who bought recently. A seller who purchased in 2020 or 2021 and needs to net a specific number may be squeezed by current pricing. A seller who purchased in 2000 for $250,000 and has a home worth $650,000 today has significant pricing flexibility - they can price correctly for the current market, present the home well, and still walk away with a net that transforms their financial picture.

The key insight for longtime owners considering downsizing: you don't need the 2022 peak price to make this work financially. The appreciation that has accumulated over fifteen or twenty years of ownership in these zip codes is so significant that current pricing, even below peak, still produces outcomes that would have seemed extraordinary when you bought. The question is not whether you can get the 2022 price. The question is whether what you'll net in the current market is enough to fund the next chapter you're planning.

For most longtime owners in 78750 and 78759, the honest answer to that question is yes.

The Sequencing Question: Sell First or Buy First?

This is the question that comes up in almost every downsizing conversation, and it doesn't have a single right answer. It depends on your financial situation, your risk tolerance, your timeline, and what the specific next home looks like.

The case for selling first: you know exactly what you're working with. You close on your current home, you have your net proceeds, and you go looking for your next place with cash in hand and no contingency hanging over your head. In a market where sellers of smaller homes, condos, or townhomes may be reluctant to accept offers contingent on another sale, coming in clean is a genuine advantage. The downside is the gap between closing dates - you may need to rent temporarily or negotiate a leaseback from your buyer, which adds logistical complexity.

The case for buying first: you find the right next home before you sell, you don't have to move twice, and you avoid the pressure of needing to find something quickly after your home closes. The downside is financial exposure - you're carrying two mortgages or two sets of carrying costs until the current home sells, and that can create stress if the current home doesn't sell on your timeline.

The bridge approach - using a bridge loan or HELOC to fund the purchase of the next home before the current one closes - is a middle path that some sellers in this price range use effectively. It requires sufficient equity in the current home (which most longtime 78750 and 78759 owners have) and a lender relationship. It's worth discussing with your financial advisor and lender if the sequencing question is creating hesitation.

For most longtime owners in these zip codes who are not under financial pressure, selling first or simultaneously tends to produce better outcomes than buying first without a clear buyer for the current home. The main exception is if you've found a specific property that is genuinely right for your next chapter and you risk losing it. In that case, the cost of carrying both properties briefly may be worth the certainty of the next home.

What People Don’t Know About Downsizing in Northwest Austin

What Downsizing Actually Costs: The Numbers Most People Underestimate

Going into a downsizing decision with accurate numbers about what it costs to sell is important, because the net proceeds from your sale are the foundation everything else is built on.

Selling costs in 78750 and 78759 typically run 8% to 10% of the gross sale price when you account for broker commissions, title insurance, escrow fees, any seller concessions or repairs negotiated during the transaction, and staging and pre-listing preparation. On a $650,000 home, that's $52,000 to $65,000 in transaction costs. On a $750,000 home, $60,000 to $75,000.

Capital gains exposure beyond the federal exclusion, if any, needs to be calculated with your CPA based on your specific purchase price, improvements made during ownership, and current income level.

Moving costs, temporary storage if needed, and the cost of setting up the new place - whether that's new furniture, window treatments, or modifications to the next home - add up quickly and are often underestimated. Budget a realistic number for this rather than assuming it will be minimal.

On the buy side, the smaller home or condo or townhome you're moving into comes with its own transaction costs - typically 2% to 3% of the purchase price including inspection, title, and lender fees if you're financing. If the next home has HOA dues, those become an ongoing carrying cost that doesn't exist if your current home is non-HOA.

None of this is a reason not to downsize - for most longtime owners in these zip codes, the equity unlock is large enough that the transaction costs are a fraction of what they're netting. But going in with accurate numbers means you make decisions based on reality rather than discovering a gap after you're under contract.

What If Your Northwest Austin Home Needs Too Much Work to Sell?

What Longtime 78750 and 78759 Owners Are Typically Weighing

The financial case for downsizing from these zip codes is often straightforward. The harder part for most longtime owners is the non-financial side of the decision.

The neighborhood connection is real. If you've lived in Spicewood Estates, Balcones Woods, Canyon Creek, or one of the other 78750 or 78759 neighborhoods for twenty years, you have relationships, routines, and roots that don't automatically transfer to a new location. The coffee shop you've been going to, the neighbors you know by name, the familiarity with every shortcut and every good dinner spot - those are worth something. They're not infinite in value, but they're not zero either, and sellers who feel ambivalent about leaving their neighborhood tend to be more satisfied with their decision when they've honestly accounted for what they're giving up rather than treating it as irrelevant.

The maintenance reality often tips the scale. A 3,000 square foot home built in 1992 requires ongoing attention that many homeowners are increasingly less interested in managing. The HVAC service calls, the roof inspection after every hail storm, the foundation monitoring, the gutters, the pool equipment if there's a pool, the yard and landscaping. As that list grows relative to what you want to be doing with your time, the appeal of a smaller home with less maintenance - or a condo or townhome where the exterior is someone else's responsibility - becomes more concrete.

The one-story question matters specifically to this age group. A two-story home that worked perfectly well when everyone was younger starts to feel like a practical compromise as knees and hips become more of a conversation. The stairs aren't a crisis - they're just something that starts to register in the back of the mind. One-story homes in 78750 and 78759 are available but represent a smaller subset of the inventory. This is sometimes the catalyst that moves a vague downsizing thought into a specific search.

The Timing Question: Is Now the Right Time?

Sellers who have been waiting for the market to return to 2022 peak levels before downsizing have been waiting for a few years now, and some of them have accumulated carrying costs and deferred maintenance in the process. Whether that wait has been worth it depends entirely on what prices do from here - and that's a question nobody can answer with certainty.

What can be said: 78750 and 78759 have held value better than most Austin zip codes through the post-peak correction. The underlying demand drivers - employer base, school feeders, established infrastructure - are still intact. The market is functional for sellers who price correctly and present well. Longtime owners with substantial equity don't need a peak market to accomplish their financial goals.

The question to ask is not "is this the best possible market to sell in?" - because you can't know the answer to that in advance. The question is "is this market good enough that selling now makes sense for my situation?" For most longtime owners in these zip codes who are genuinely ready to downsize, the answer is probably yes. The cost of waiting for a market that may or may not return on a useful timeline is real - in maintenance costs, in opportunity cost of deployed equity, and in the time spent in a home that doesn't fit anymore.

The other timing consideration is personal rather than market-driven. The best time to downsize is generally while you have full energy and discretion to manage the process - while you can still drive the decisions about what to keep, where to donate, how to manage the move, and what kind of home you want next. Waiting until a health event or a life disruption forces the decision means making those choices under pressure rather than from a position of choice.

When Is the Right Time to Downsize Your Northwest Austin Home?

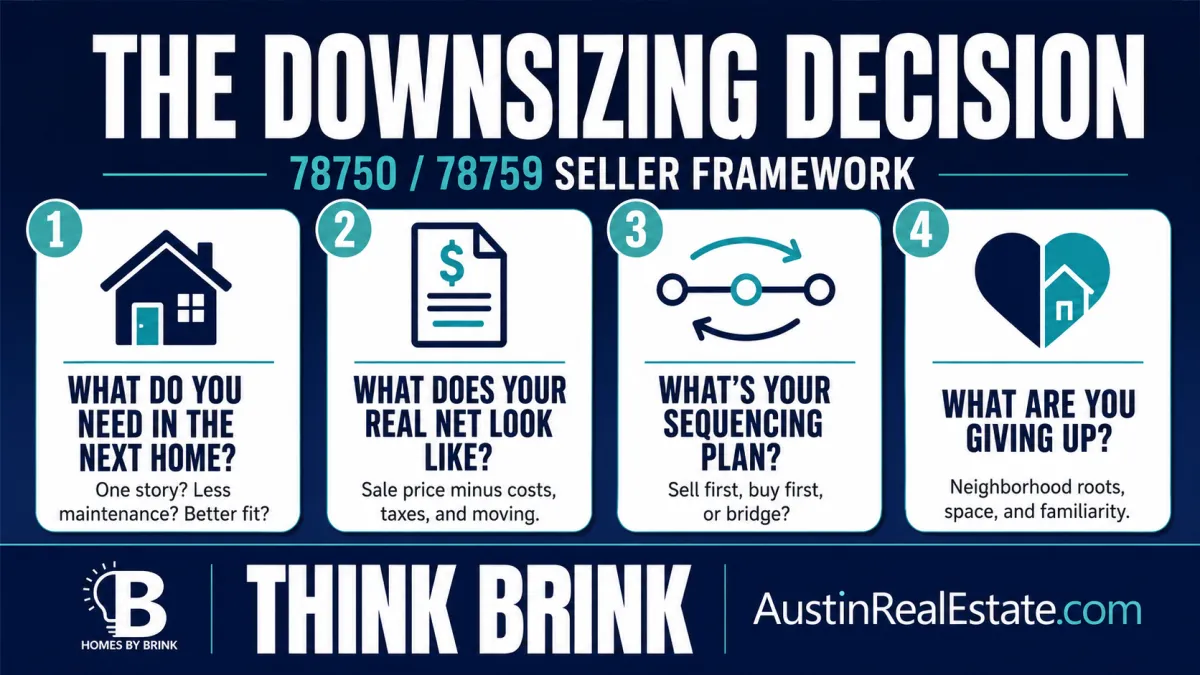

The Questions Worth Answering Before You List

If you're a longtime 78750 or 78759 homeowner seriously considering a downsize, here are the questions worth working through before you call an agent:

What do you actually need from the next home? One story, certain square footage, specific location relative to family or medical providers or the neighborhoods you want to stay close to, HOA maintenance vs no HOA, proximity to what you use most in your daily life. The clearer you are on this before you start looking, the better the decision you'll make.

What does your real net look like? Get an honest current market value estimate for your home, apply realistic transaction costs, account for any capital gains exposure with your CPA, and arrive at an actual net number. Then figure out what that buys in the next home category you're targeting. This math needs to be done before you fall in love with a specific next home.

Do you have the over-65 school tax freeze, and have you planned for the Tax Ceiling Certificate transfer? If you're 65 or older and have the freeze on your current home, make sure your agent and title company know to get the certificate at closing, and apply it to the new property within one year.

What's your sequencing plan? Sell first, buy first, or bridge? Know the answer before you get into contract on either side.

What are you giving up by leaving, and is the trade worth it? Not a trick question - it's a real one. The neighborhoods in 78750 and 78759 are genuinely good places to live, and the decision to leave deserves honest consideration of what goes with the house, not just what gets unlocked financially.

What Costs Should You Expect When Downsizing in Texas?

Should You Hire a Senior Move Manager When Downsizing in Austin?

How to Talk With Adult Children About Selling the Family Home

The Honest Summary

For most longtime owners in 78750 and 78759, the financial case for downsizing is strong. The equity position is significant, the market is functional, the tax situation is manageable with proper planning, and the next home category - whether that's a smaller single-family, a townhome, or a low-maintenance condo - is well represented in the Austin metro.

The decision is ultimately personal, not financial. The finances usually work. The question is whether you're ready, whether the timing makes sense for your life situation, and whether you've done the homework on what the next chapter actually looks like rather than just what you're leaving behind.

Sellers who go into a downsizing move with clear numbers, a realistic plan for sequencing, and an honest accounting of what they want in the next home tend to feel good about the decision - sometimes immediately, sometimes after the dust settles and they're living in a space that actually fits. The ones who struggle are usually the ones who moved before they were clear on where they were going, or who sold under pressure without adequate preparation.

If you're somewhere in the middle of thinking this through, that's a completely normal place to be. The conversation is worth having before you've decided rather than after.

Frequently Asked Questions

Do I have to pay capital gains tax when I sell my 78750 or 78759 home?

Married couples can exclude up to $500,000 in capital gains from federal income tax when selling a primary residence they've lived in for at least two of the past five years. Single filers can exclude up to $250,000. For many longtime 78750 and 78759 owners, this exclusion covers all or most of the gain. Gains above the exclusion are subject to capital gains tax at rates that depend on your income level. Consult a CPA for your specific situation before making timing decisions around this.

If I have the Texas over-65 school tax freeze, do I lose it when I downsize?

No - you can transfer it. When you sell, request a Tax Ceiling Certificate from your county appraisal district. Present it to the new county's appraisal district within one year of your move. The freeze transfers proportionally to the new property. This is a specific Texas provision that many downsizing homeowners don't know about and that meaningfully affects the long-term carrying cost of the next home.

What are the new Texas over-65 property tax exemptions as of 2026?

As of January 1, 2026, eligible Texas homeowners age 65 or older can combine a $140,000 general homestead exemption with a $60,000 over-65 exemption, for a total $200,000 reduction in taxable value for school tax purposes. For many homes in these zip codes, this effectively eliminates school district taxes for qualifying owners. Apply with your county appraisal district using Form 50-114.

Should I sell my 78750 or 78759 home before I buy the next one, or buy first?

Selling first gives you certainty about your net proceeds and lets you make a clean offer on the next home without a sale contingency. Buying first avoids a temporary housing gap but creates financial exposure if your current home takes longer to sell. For most longtime owners in these zip codes with substantial equity and no pressing timeline, selling first or simultaneously tends to reduce risk. The exception is if you've found a specific next home you're at risk of losing.

How much does it cost to sell a home in 78750 or 78759?

Total transaction costs typically run 8% to 10% of the gross sale price, including broker commissions, title insurance, escrow fees, any seller concessions or repairs, and pre-listing preparation including staging and photography. On a $650,000 home that's approximately $52,000 to $65,000. Factor this into your net proceeds calculation before you make decisions about what the next home can cost.

Is the current market good enough to downsize into, or should I wait?

78750 and 78759 have held value better than most Austin zip codes through the post-peak correction. Homes are selling in the current market for sellers who price correctly and present well. Longtime owners with substantial equity don't need a peak market to accomplish their financial goals. Whether to wait depends on your personal situation and timeline, not on whether a peak market might return.

What should I look for in a next home when downsizing from 78750 or 78759?

The most common priorities for downsizers from these zip codes are single-story layout, lower maintenance - either through smaller square footage or an HOA that handles exterior upkeep - proximity to the neighborhoods and services they're used to, and a price point that meaningfully reduces carrying costs relative to the current home. The specific mix depends entirely on your situation, which is why clarity on what you actually need in the next chapter matters before you start looking.